A down payment on a home also safeguards you as the purchaser. If you wish to offer your house and the market drops, you might owe more on your property than it's worth. If you made a bigger deposit when you acquired your house you might break even, or perhaps generate income when you sell.

Nevertheless, the four typical are: With this kind of mortgage, you keep the very same interest rate for the life of the loan, which means the principal and interest portion of your monthly home mortgage payment remains the very same (what does ltv stand for in mortgages). These kinds of loans generally are available in 10, 15, 20 or 30-year terms.

The most common way to cover this cost is to spend for it in a regular monthly premium that's contributed to your mortgage payment. PMI generally equals 1% of your loan balance each year. Many lending institutions offer traditional loans with PMI for down payments as low as 5%, and some as low as 3%.

The down payment is usually between 3 and 20%, and will require PMI for buyers who put down less than 20%. With an ARM, the initial rate is often lower than a fixed-rate loan - what is the interest rates on mortgages. However, the interest rate may go up with time. This is a kind of loan guaranteed by the federal government.

5%. Unlike standard home loans, home mortgage insurance coverage includes both an in advance quantity and a monthly premium. This type of loan is just readily available for U.S. military veterans and active-duty servicemembers. VA loans are funded by a loan provider and guaranteed by the Department of Veterans Affairs. The main benefit of pursuing this type of loan is it might not need a deposit.

Some Known Details About What Is The Interest Rate Today For Mortgages

Purchasers with credit report as low as 500 might still be able to get a loan for a house, however they'll likely face greater rates of interest and have fewer options. The higher your credit history, the lower your rates of interest. A strong credit score also means lending institutions are more likely to be lax in locations where you may not be as strong, such as your deposit.

In these instances, they might allow you to get a great rates of interest while making a smaller sized down payment. If you have the ability to do so, timeshares wikipedia you may want to think about putting down a payment that's bigger than 20%. Here are some of the benefits: Lower month-to-month payment due to no mortgage insurance and smaller loan amount Less interest paid over the life of the loan More versatility if you require to offer on short notice Just how much do you require for a deposit, then? Use an affordability calculator to determine just how much you must save prior to buying a house.

You can change the loan terms to see additional price, loan and deposit quotes. Here are some actions you can take previously identifying just how much house you can manage and just how much you can put down on a house: Evaluation your existing spending plan to figure out just how much you can manage, and just how much you desire to spend.

Ask yourself what you truly need from your home. For instance, do you prepare to begin a household? Do you have teens who will soon be moving out? These are very important factors to consider. You need to expect not only the phase of life you remain in today, but likewise what phase you'll be going into while in your house.

You may need to search for a loan alternative that allows a smaller sized down payment, or you might want to give yourself more time to save up for a bigger deposit. It can be helpful to deal with someone who understands the responses to all these concerns. A can help you comprehend the different kinds of mortgages readily available and discuss down payment requirements for each type https://travelexperta.com/2020/09/what-to-look-for-in-a-quality-real-estate-agent.html of loan to find the best one for your monetary situation.

Our How To Calculate Interest Only Mortgages Statements

Usually, buyers put down 5 to 20% of the purchase rate but this can be as little as 3%. Purchasers putting down less than 20% are needed to pay Personal Mortgage Insurance coverage (PMI) regular monthly till they develop 20% equity in their house.

A deposit is a portion of the expense of a home, paid up front. Generally, the more you put down, the lower your interest rate and month-to-month payment. Why? Because the deposit is efficiently your investment in your house. When you put more cash down, you're taking on a part of danger from the lending institution, who can reciprocate by offering you possibly lower home loan rates of interest.

Some government-backed loans, like FHA mortgages, VA loans, and USDA loans might be offered to qualified house buyers with little or no down payment. However, with a few of these loan programs, you might be needed to pay for mortgage insurance coverage an extra regular monthly expenditure you'll require to pay in addition to your mortgage payment.

Because the quantity of your deposit is deducted from the overall cost of a home, your loan amount will be smaller sized with a bigger down payment therefore will your monthly payments. You can use our deposit calculator to approximate your month-to-month payments based on the quantity you obtain.

A larger deposit might get you into a more pricey home or a lower rate of interest. Nevertheless, there are factors you may want to put down less. Let's take a look at how your down payment impacts the terms of your loan. The larger the deposit you provide your home mortgage loan provider, the lower your interest rate may be.

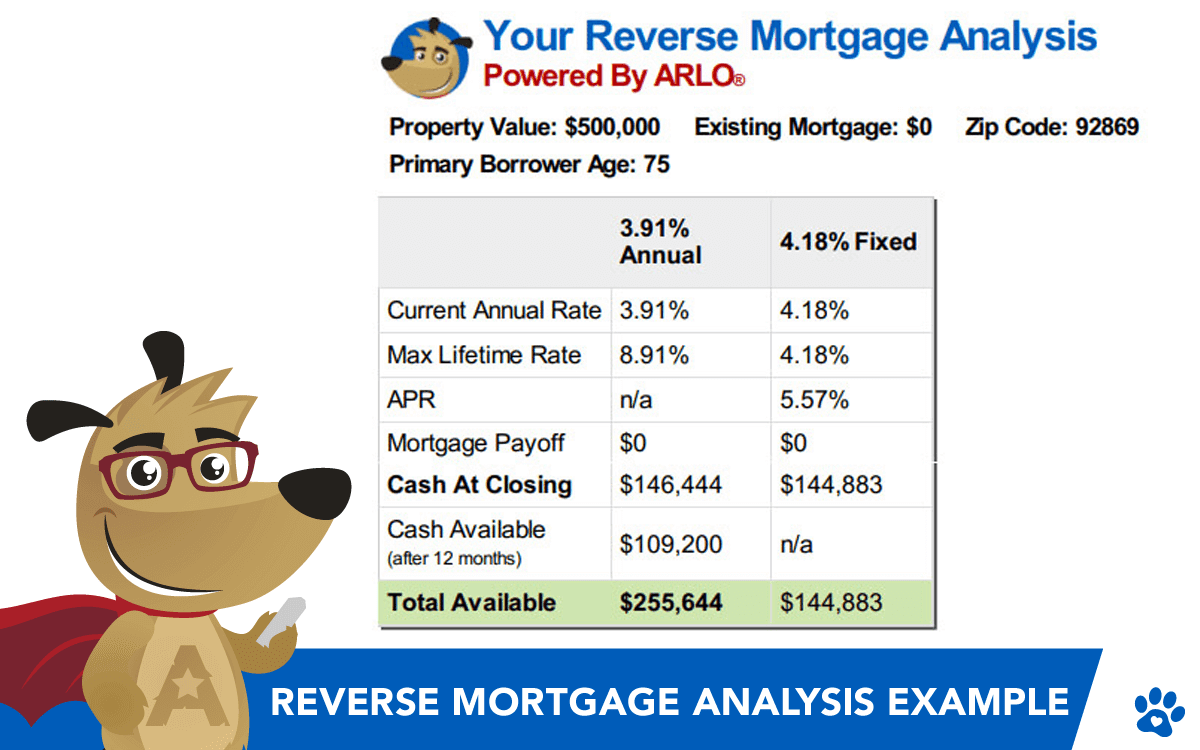

How Do Banks Make Money On Reverse Mortgages - An Overview

A lower rates of interest will help you save on your regular monthly payment and allow you to pay less interest over the life of the loan. A bigger down payment usually implies smaller sized month-to-month payments. Given that the balance of your loan is less, your regular monthly payments are smaller. Let's state you desire to acquire a $300,000 home with a deposit of 10% ($ 30,000) on a 30-year mortgage.

Without considering interest, taxes or insurance, your regular monthly payment in this example would have to do nick weiser with $750. Now, let's state that you put down 20% instead. This would reduce the primary amount on your loan to $240,000. On a 30-year home loan, your regular monthly payment would be about $667 (omitting interest, taxes or insurance coverage).

That may not appear like much, but it's also not the complete image. A 20% deposit could save you numerous dollars a month on home mortgage insurance coverage, and it might likewise indicate a better rates of interest. To look at how a deposit affects your month-to-month home loan payment, attempt a home loan calculator.

A deposit is the cash you'll put down during your mortgage closing, which is the last action you'll take when purchasing a home. Throughout the closing, you'll likewise sign your home mortgage documents and formally get ownership of the home. Lenders often express your deposit as a percentage. For example, a 20% down payment on a $200,000 mortgage suggests you'll pay $40,000 when you close on your loan.